The Discipline of Rebalancing: Why Portfolios Drift and What to Do About It

A portfolio is not a "set it and forget it" object. Left alone, it drifts.

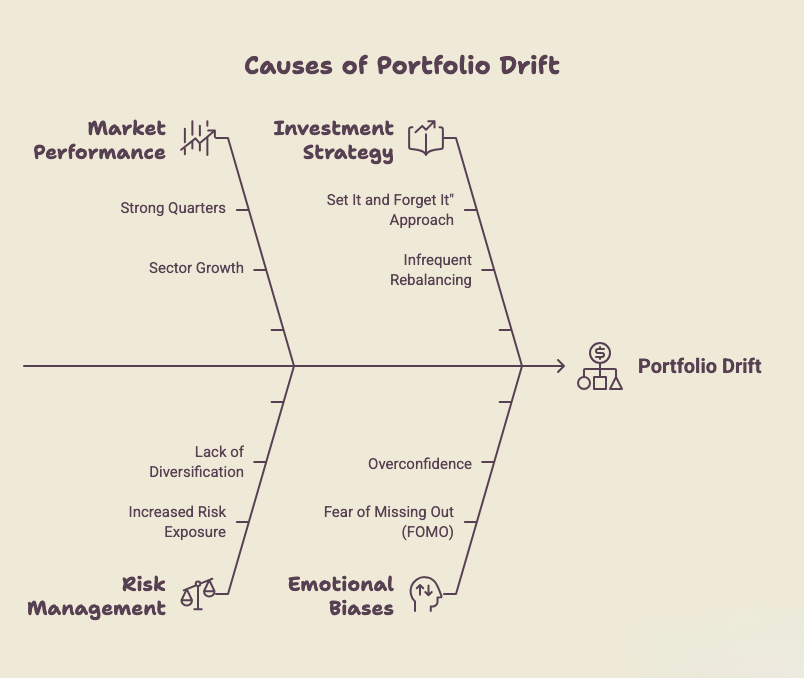

When one part of the market runs ahead of the rest, the positions that grew fastest quietly become a larger share of your total portfolio. Nobody made a decision to take on more risk. The market made it for you, one strong quarter at a time.

That's the core problem rebalancing solves. It's the discipline of periodically bringing a portfolio back toward the mix you originally intended, rather than letting recent performance dictate your risk level.

Why drift matters

Say you build a portfolio targeting a specific split between growth-oriented and income-oriented holdings. A few years of strong performance in the growth side can shift that split meaningfully without a single new purchase. The portfolio still looks fine on the surface. Balances are up. But the risk profile underneath has changed, often without the investor noticing until a downturn makes it obvious.

How direct ownership changes the mechanics

When a portfolio is built from individual securities rather than only pooled funds, rebalancing becomes a more precise exercise. An adviser can look at specific positions and specific tax lots, not just fund-level allocations, and make more granular decisions about what to trim and when.

That precision also opens the door to coordinating rebalancing with tax planning. Trimming a position that has a loss can offset gains elsewhere. Trimming a position with a long-term gain can sometimes be timed around a lower-income year. None of this is guaranteed to improve outcomes, and it depends heavily on individual circumstances, but it's a level of control that a standardized fund portfolio doesn't offer in the same way.

What rebalancing is not

Rebalancing is not market timing. It doesn't attempt to predict what will happen next. It's the opposite instinct: a systematic check that keeps a portfolio aligned with a plan, regardless of what the market has been doing lately.

It's also not free. Selling appreciated positions can trigger taxable gains, and transaction costs matter. A disciplined rebalancing approach weighs the benefit of staying aligned with your target allocation against the cost of getting there.

The bottom line

Most investors think about what to buy. Fewer think systematically about when to trim what's already worked. Rebalancing is a maintenance habit, not a one-time decision, and it's one of the more overlooked disciplines in long-term portfolio management.

When did you last check whether your portfolio still reflects the mix you intended, or the mix the market has built for you?

Informational purposes only. Not investment, tax, or legal advice. Rebalancing does not guarantee a profit or protect against loss, and all investing involves risk, including possible loss of principal. Consult a qualified tax professional regarding your specific situation. William Allan is an investment adviser registered with the SEC; registration does not imply any specific level of skill or training.